HEALTHCARE

Global Teleradiology Market - Industry Trends and Forecast to 2032

REPORT OVERVIEW

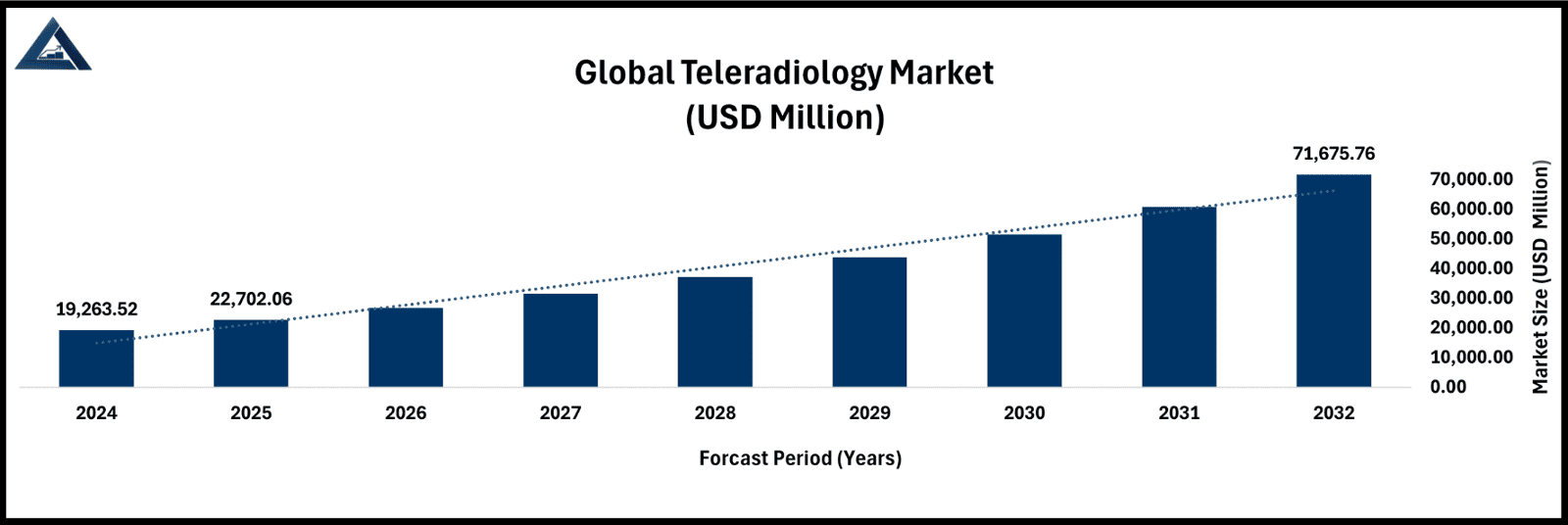

Global Teleradiology Market – Insights on Industry Trends and Forecast to 2032: An In-Depth Analysis by Component (Teleradiology Services, Software, Hardware, Telecom and Networking), Imaging Technique (Computed Tomography, Magnetic Resonance Imaging, Ultrasound, X-Ray, Mammography, Nuclear Imaging, and Fluoroscopy), End-user (Hospitals and Clinics, Diagnostic Imaging Centers and Laboratories, Long-Term Care Centers, Nursing Homes & Assisted Living Facilities, and Others), Report Type (Preliminary Reports and Final Reports), Specialty (Cardiology, Neurology, Oncology, Musculoskeletal, Gastroenterology, and Others), and Region (North America, Europe, Asia-Pacific, South America, Middle East and Africa)

Market Insights

To learn more about this report, Request a free sample copy.

RESEARCH FOCUS & KEY INSIGHTS DELIVERED

SEGMENTATION

- Component

- Teleradiology Services

- Software

- Picture Archiving and Communications Systems

- Radiology Information Systems

- Hardware

- Telecom and Networking

- Web- Based Tele Radiology Solutions

- Cloud- Based Tele Radiology Solutions

- Imaging Technique

- Computed Tomography

- Magnetic Resonance Imaging

- Ultrasound

- X-Ray

- Mammography

- Nuclear Imaging

- Fluoroscopy

- End-user

- Hospitals and Clinics

- Diagnostic Imaging Centers and Laboratories

- Long-Term Care Centers

- Nursing Homes & Assisted Living Facilities

- Others

- Report Type

- Preliminary Reports

- Final Reports

- Specialty

- Cardiology

- Neurology

- Oncology

- Musculoskeletal

- Gastroenterology

- Others

REGIONAL SEGMENTATION

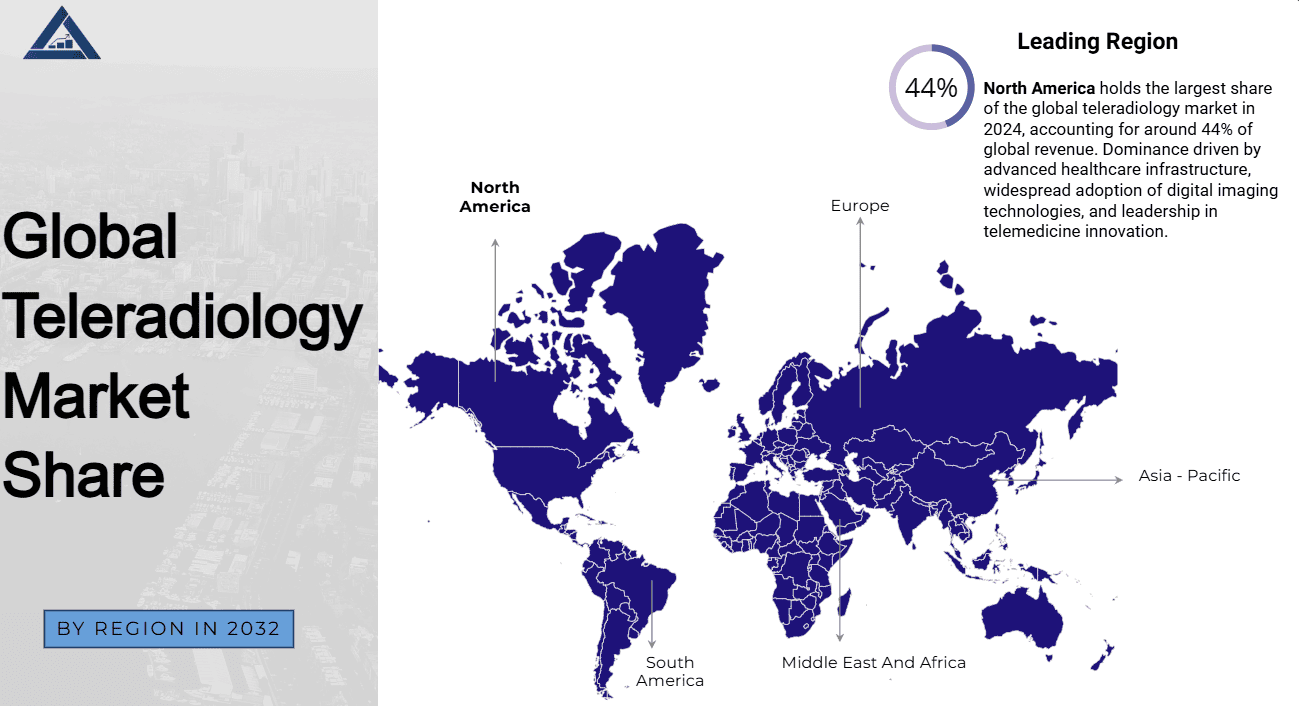

North America holds a dominant portion of the worldwide teleradiology market, representing nearly 44% of the overall market. This strong market position is supported by the growing need for off-site diagnostic solutions, an expanding elderly population, and the escalating prevalence of long-term medical conditions across the U.S. and Canada. The region’s commitment to healthcare digitalization, along with the extensive implementation of next-generation imaging systems and integration of AI-enhanced radiological tools, are major drivers behind its continued growth. Moreover, programs focused on expanding medical reach to geographically isolated and medically underserved populations, combined with the urgent need for more rapid diagnostic procedures, are propelling the broader uptake of tele-radiology solutions. Supportive regulatory policies, a robust virtual care network, and heavy investment in digital health technologies further reinforce North America's prominent standing in the global teleradiology arena.

To learn more about this report, Request a free sample copy.

- North America

- U.S.

- Canada

- Mexico

- Rest of North America

- Europe

- Germany

- U.K.

- France

- Italy

- Spain

- Russia

- The Netherlands

- Belgium

- Turkey

- Rest of Europe

- Asia-Pacific

- China

- India

- Japan

- South Korea

- Singapore

- Malaysia

- Australia

- Thailand

- Philippines

- Rest of Asia-Pacific

- South America

- Brazil

- Argentina

- Chile

- Colombia

- Rest of South America

- Middle East and Africa

- Kingdom of Saudi Arabia

- South Africa

- U.A.E.

- Egypt

- Rest of Middle East and Africa

KEY MARKET PLAYERS

- Agfa-Gevaert

- Virtual Radiologic

- Onrad Inc

- Everlight Radiology

- 4ways Healthcare Ltd.

- RamSoft, Inc.

- USARAD Holdings, Inc.

- Koninklijke Philips N.V.

- Medica Group PLC

- Teleradiology Solutions

TELERADIOLOGY MARKET SCOPE

Table OF CONTENTS

- SECTION 1 - INTRODUCTION

- 1.1 Taxonomy

- 1.2 Market Overview

- 1.3 Currency and Limitations

- 1.3.1 Currency

- 1.3.2 Limitations

- 1.4 Key Competitors

- SECTION 2 - RESEARCH METHODOLOGY

- 2.1 Research Approach

- 2.2 Data Collection and Validation

- 2.2.1 Secondary Research

- 2.2.2 Primary Research

- 2.3 Market Assessment

- 2.3.1 Market Size Estimation

- 2.3.2 Bottom-up Approach

- 2.3.3 Top-down Approach

- 2.3.4 Growth Forecast

- 2.4 Market Study Assumptions

- 2.5 Data Sources

- SECTION 3 - EXECUTIVE SUMMARY

- 3.1 Global Teleradiology Market, by Component

- 3.2 Global Teleradiology Market, by Imaging Technique

- 3.3 Global Teleradiology Market, by End-user

- 3.4 Global Teleradiology Market, by Report Type

- 3.5 Global Teleradiology Market, by Specialty

- 3.6 Global Teleradiology Market, by Geography

- 3.7 Market Position Grid

- SECTION 4 - PREMIUM INSIGHTS

- 4.1 Regulatory Framework

- 4.1.1 Standards

- 4.1.2 Regulatory Landscape

- 4.2 Value Chain Analysis

- 4.3 Supply Chain Analysis

- 4.4 COVID-19 Impact

- 4.5 Russia-Ukraine War Impact

- 4.6 PORTER's Five Force Analysis

- 4.7 PESTLE Analysis

- 4.8 SWOT Analysis

- 4.9 Go to Market Strategy

- 4.10 Opportunity Orbit

- 4.11 Multivariate Modelling

- 4.12 Pricing Analysis

- SECTION 5 - MARKET DYNAMICS

- 5.1 Trends

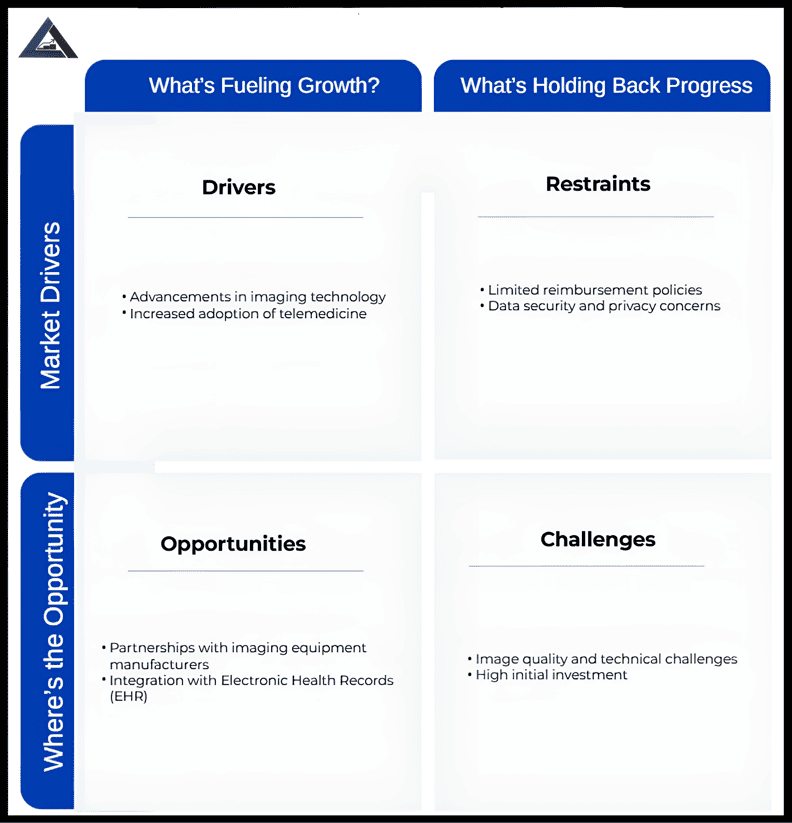

- 5.1.1 Increased focus on subspecialty teleradiology

- 5.1.2 Blockchain for secure data sharing

- 5.1.3 Trend 3

- 5.2 Drivers

- 5.2.1 Advancements in imaging technology

- 5.2.2 Increased adoption of telemedicine

- 5.2.3 Driver 3

- 5.2.4 Driver 4

- 5.3 Restraints

- 5.3.1 Limited reimbursement policies

- 5.3.2 Data security and privacy concerns

- 5.3.3 Restraint 3

- 5.4 Opportunities

- 5.4.1 Partnerships with imaging equipment manufacturers

- 5.4.2 Integration with Electronic Health Records (EHR)

- 5.4.3 Opportunity 3

- 5.4.4 Opportunity 4

- 5.5 Challenges

- 5.5.1 Image quality and technical challenges

- 5.5.2 High initial investment

- 5.5.3 Challenge 3

- SECTION 6 - GLOBAL TELERADIOLOGY MARKET, BY COMPONENT

- 6.1 Component Summary

- 6.2 Market Attractive Index

- 6.3 Global Teleradiology Market, by Component (2019-2032)

- SECTION 7 - GLOBAL TELERADIOLOGY MARKET, BY IMAGING TECHNIQUE

- 7.1 Imaging Technique Summary

- 7.2 Market Attractive Index

- 7.3 Global Teleradiology Market, by Imaging Technique (2019-2032)

- SECTION 8 - GLOBAL TELERADIOLOGY MARKET, BY END-USER

- 8.1 End-user Summary

- 8.2 Market Attractive Index

- 8.3 Global Teleradiology Market, by End-user (2019-2032)

- SECTION 9 - GLOBAL TELERADIOLOGY MARKET, BY REPORT TYPE

- 9.1 Report Type Summary

- 9.2 Market Attractive Index

- 9.3 Global Teleradiology Market, by Report Type (2019-2032)

- SECTION 10 - GLOBAL TELERADIOLOGY MARKET, BY SPECIALTY

- 10.1 Specialty Summary

- 10.2 Market Attractive Index

- 10.3 Global Teleradiology Market, by Specialty (2019-2032)

- SECTION 11 - GLOBAL TELERADIOLOGY MARKET, BY GEOGRAPHY

- 11.1 Regional Summary

- 11.2 Market Attractive Index

- 11.3 Global Teleradiology Market, by Geography (2019-2032)

- SECTION 12 - NORTH AMERICA TELERADIOLOGY MARKET

- 12.1 North America Summary

- 12.2 Market Attractive Index

- 12.3 North America Teleradiology Market, by Component (2019-2032)

- 12.4 North America Teleradiology Market, by Imaging Technique (2019-2032)

- 12.5 North America Teleradiology Market, by End-user (2019-2032)

- 12.6 North America Teleradiology Market, by Report Type (2019-2032)

- 12.7 North America Teleradiology Market, by Specialty (2019-2032)

- 12.8 North America Teleradiology Market, by Country (2019-2032)

- 12.8.1 U.S.

- 12.8.2 Canada

- 12.8.3 Mexico

- 12.8.4 Rest of North America

- SECTION 13 - EUROPE TELERADIOLOGY MARKET

- 13.1 Europe Summary

- 13.2 Market Attractive Index

- 13.3 Europe Teleradiology Market, by Component (2019-2032)

- 13.4 Europe Teleradiology Market, by Imaging Technique (2019-2032)

- 13.5 Europe Teleradiology Market, by End-user (2019-2032)

- 13.6 Europe Teleradiology Market, by Report Type (2019-2032)

- 13.7 Europe Teleradiology Market, by Specialty (2019-2032)

- 13.8 Europe Teleradiology Market, by Country (2019-2032)

- 13.8.1 Germany

- 13.8.2 U.K.

- 13.8.3 France

- 13.8.4 Italy

- 13.8.5 Spain

- 13.8.6 Russia

- 13.8.7 The Netherlands

- 13.8.8 Belgium

- 13.8.9 Turkey

- 13.8.10 Rest of Europe

- SECTION 14 - ASIA-PACIFIC TELERADIOLOGY MARKET

- 14.1 Asia-Pacific Summary

- 14.2 Market Attractive Index

- 14.3 Asia-Pacific Teleradiology Market, by Component (2019-2032)

- 14.4 Asia-Pacific Teleradiology Market, by Imaging Technique (2019-2032)

- 14.5 Asia-Pacific Teleradiology Market, by End-user (2019-2032)

- 14.6 Asia-Pacific Teleradiology Market, by Report Type (2019-2032)

- 14.7 Asia-Pacific Teleradiology Market, by Specialty (2019-2032)

- 14.8 Asia-Pacific Teleradiology Market, by Country (2019-2032)

- 14.8.1 China

- 14.8.2 India

- 14.8.3 Japan

- 14.8.4 South Korea

- 14.8.5 Singapore

- 14.8.6 Malaysia

- 14.8.7 Australia

- 14.8.8 Thailand

- 14.8.9 Philippines

- 14.8.10 Rest of Asia-Pacific

- SECTION 15 - SOUTH AMERICA TELERADIOLOGY MARKET

- 15.1 South America Summary

- 15.2 Market Attractive Index

- 15.3 South America Teleradiology Market, by Component (2019-2032)

- 15.4 South America Teleradiology Market, by Imaging Technique (2019-2032)

- 15.5 South America Teleradiology Market, by End-user (2019-2032)

- 15.6 South America Teleradiology Market, by Report Type (2019-2032)

- 15.7 South America Teleradiology Market, by Specialty (2019-2032)

- 15.8 South America Teleradiology Market, by Country (2019-2032)

- 15.8.1 Brazil

- 15.8.2 Argentina

- 15.8.3 Chile

- 15.8.4 Colombia

- 15.8.5 Rest of South America

- SECTION 16 - MIDDLE EAST AND AFRICA TELERADIOLOGY MARKET

- 16.1 Middle East and Africa Summary

- 16.2 Market Attractive Index

- 16.3 Middle East and Africa Teleradiology Market, by Component (2019-2032)

- 16.4 Middle East and Africa Teleradiology Market, by Imaging Technique (2019-2032)

- 16.5 Middle East and Africa Teleradiology Market, by End-user (2019-2032)

- 16.6 Middle East and Africa Teleradiology Market, by Report Type (2019-2032)

- 16.7 Middle East and Africa Teleradiology Market, by Specialty (2019-2032)

- 16.8 Middle East and Africa Teleradiology Market, by Country (2019-2032)

- 16.8.1 Kingdom of Saudi Arabia

- 16.8.2 South Africa

- 16.8.3 U.A.E.

- 16.8.4 Egypt

- 16.8.5 Rest of Middle East and Africa

- SECTION 17 - COMPANY SHARE ANALYSIS

- 17.1 Global Teleradiology Market, Company Share Analysis

- 17.2 North America Teleradiology Market, Company Share Analysis

- 17.3 Europe Teleradiology Market, Company Share Analysis

- 17.4 Asia-Pacific Teleradiology Market, Company Share Analysis

- SECTION 18 - COMPANY PROFILES

- 18.1 Agfa-Gevaert

- 18.1.1 Company Snapshot

- 18.1.2 Financial Overview

- 18.1.3 Product Portfolio

- 18.1.4 Recent Developments

- 18.2 Virtual Radiologic

- 18.2.1 Company Snapshot

- 18.2.2 Financial Overview

- 18.2.3 Product Portfolio

- 18.2.4 Recent Developments

- 18.3 Onrad Inc

- 18.3.1 Company Snapshot

- 18.3.2 Financial Overview

- 18.3.3 Product Portfolio

- 18.3.4 Recent Developments

- 18.4 Everlight Radiology

- 18.4.1 Company Snapshot

- 18.4.2 Financial Overview

- 18.4.3 Product Portfolio

- 18.4.4 Recent Developments

- 18.5 4ways Healthcare Ltd.

- 18.5.1 Company Snapshot

- 18.5.2 Financial Overview

- 18.5.3 Product Portfolio

- 18.5.4 Recent Developments

- 18.6 RamSoft, Inc.

- 18.6.1 Company Snapshot

- 18.6.2 Financial Overview

- 18.6.3 Product Portfolio

- 18.6.4 Recent Developments

- 18.7 USARAD Holdings, Inc.

- 18.7.1 Company Snapshot

- 18.7.2 Financial Overview

- 18.7.3 Product Portfolio

- 18.7.4 Recent Developments

- 18.8 Koninklijke Philips N.V.

- 18.8.1 Company Snapshot

- 18.8.2 Financial Overview

- 18.8.3 Product Portfolio

- 18.8.4 Recent Developments

- 18.9 Medica Group PLC

- 18.9.1 Company Snapshot

- 18.9.2 Financial Overview

- 18.9.3 Product Portfolio

- 18.9.4 Recent Developments

- 18.10 Teleradiology Solutions

- 18.10.1 Company Snapshot

- 18.10.2 Financial Overview

- 18.10.3 Product Portfolio

- 18.10.4 Recent Developments

- SECTION 19 - RELATED REPORTS

- SECTION 20 - DISCLAIMER

RESEARCH METHODOLOGY

RESEARCH AND DATA COLLECTION

- Research articles published on Technium

- Science and MDPI

- Research publications by government approved associations and societies

DATA PRE-PROCESSING

The term "data pre-processing" refers to the collection of procedures and methods used to clean, modify, and make ready for analysis the raw data gathered during research and data collection. The completion of this phase is necessary to guarantee that the data are reliable, consistent, and appropriate for statistical analysis and other data-driven tasks. The data pre-processing ensures that the information gathered from research and data collection is comparable and expressed in standard units, by the integration of missing data pointers and algorithmic approaches.

MODELING AND FORECASTING

QUALITY ASSURANCE AND OUTPUT

Quality assurance and output involves the process of validation, adjustments, further publications of key market indicators. Extensive plausibility and consistency tests are performed on derived time series to ensure the high degree of quality of our market analysis. This quality assurance procedure also includes rigorous inspection, validation, and editing by an experienced management team to assure the dependability of the published data.